This handbook endeavours to answer all your questions about IMRO. It covers such topic as:

- how membership works and the different grades of membership,

- what you need to know about repertoire and notifying IMRO when you have written something new,

- music licensing in Ireland;

- and the details of how royalties are collected and distributed both in Ireland and abroad.

Membership

Section A – Membership

| Category | Provisional Member | Associate Member | Full Member (3) |

| Minimum Qualifying Criteria(1) (2) | After 1 year’s provisional membership aggregate earnings of €952.30 (writer) and €3,809.21 (publisher) over a period not exceeding three continuous years.(4) (For transfer members, earnings while at your previous PRO will be counted.) | After 1 year’s membership aggregate earnings of €6,348.69 (writer) and €25,394.76 (publisher) over a period not exceeding three continuous years (4) (For transfer members, earnings at your previous PRO will be counted.) | |

| Rights | (i) Receive Report & Accounts (ii) Attend General Meetings (iii) 1 vote on a show of hands or on a postal ballot | (i) Receive Report & Accounts (ii) Attend General Meetings (iii) Eligible to nominate or be nominated to Board (iv) 1 vote on a show of hands or 10 votes on a poll or postal ballot | (i) Receive Report & Accounts (ii) Attend General meetings (iii) Eligible to nominate or be nominated to Board (iv) 1 vote on a show of hands: 50 votes on a poll or postal ballot plus 50 additional votes if either of the under-noted criteria is fulfilled(3) (5). |

1. Discretion is retained by the Board of Directors to elect below the criteria in appropriate circumstances.

2. Promotions to Full and Associate membership are automatic. After the end of each financial year, members’ earnings are examined to determine those who qualify for promotion. They are then notified of their new member status. The new status is not lost by any subsequent decline in IMRO earnings below the level of current criteria.

3. Successors to deceased members are eligible for promotion to Full membership if they meet the same earnings criteria as publisher members. However, successors are not eligible for appointment to the Board of Directors, nor are they entitled to the fifty additional votes on a poll or postal ballot (note 5) unless also qualifying for Full membership as a writer or publisher in their own right.

4. The earnings criteria shown above are for promotions from 1996 onwards. They are reviewed every five years.

Minimum criteria for additional FULL MEMBER VOTES

5. To qualify for additional Full Member Votes, a member must have aggregate IMRO or IMRO and previous PRO earnings of 10 times the full membership criterion as at the preceding 31st December, during the 20 years or less up to the preceding 31st December. The earnings required are €63,486.90 (writer) and €253,947.60 (publisher).

Membership Requirements If you are are a Songwriter, Composer, Lyricist or an Arranger of public domain music and you fulfil ONE of the following criteria you are eligible to apply for IMRO membership:

- Have you had a piece of music broadcast on radio or TV in the past two years?

- Have you had at least 12 live performances of your music in the past two years?

- Have you had a piece of music used on a commercially available recording in the past two years?

- Is your music available on streaming or download services such as Spotify, Deezer or Apple Music?

Each applicant must also submit proof of identity in the form of a photocopy of a birth certificate, passport or driver’s licence.

Publishers In order to qualify for IMRO membership a music publisher must have a catalogue of at least 10 works, at least 5 of which must have received some form of commercial exploitation within the past two years. In addition, the writers of the 10 qualifying works must be members of IMRO, or of one of its affiliated societies.

A copy of the recordings or of the sheet music must be submitted in support of the application for the qualifying 10 works. Copies of all assignments between the applicant and the writers in respect of the works concerned must also be supplied. A sheet of the publisher’s headed notepaper should be provided.

- Individual applicants must also submit a copy of their birth certificate, passport or drivers licence.

- Partnerships must provide a copy of the partnership agreement

- Limited companies must provide a copy of the Memorandum and Articles of Association

Definitions The following definitions apply to the admission criteria:

‘Broadcast’ means transmission by a television or radio broadcasting station and/or inclusion in a cable programme.

‘Film’, which includes videograms (whether in the form of cassettes or discs) as well as cinematograph films as defined in Section 18 of the Copyright Act 1963.

‘Commercially published’ means:

made available to the public by sale or hire in graphic (sheet music) form

‘Commercially recorded’ means:

(i) the work has been released to the public on a record label, or

(ii) the work has been recorded and made available to the public by inclusion in a catalogue of a recorded music (e.g. background or mood music) library, or

(iii) the work has been recorded and transmitted by a television or radio broadcasting station or included in a cable programme, or

(iv) the work has been recorded on the soundtrack of a film which has been released for public exploitation.

Termination of Membership Provisional and Associate writer membership may be terminated if no royalties at all are credited to the writer over a five year period. Provisional publisher members whose royalties have not exceeded an aggregate of €317.43 over five years may also be terminated.

Successors to Deceased Members Copyright in musical works lasts for the lifetime of the author (or in the case of co-written works, the lifetime of the last surviving contributor) and for 70 years following their death.

On the death of a member, IMRO should be notified as soon as possible so that it can be established to whom future royalties should be paid. Under the company’s Articles of Association membership of IMRO ceases upon death. IMRO will continue to pay royalties to the deceased members’ executors until December 31st of the seventh year following their death, or until a successor member is admitted, whichever is the earlier.

IMRO will admit to Successor membership persons eligible under the Articles of Association. Admission is carried out in such a way as to cause the royalties to be paid in accordance with the will or operation of law. Whatever arrangements are made, IMRO is strictly accountable to pay royalties to the executors in the first instance and then to the Successor member, if one is elected. If the deceased does not leave a will, the law prescribes who is to inherit his or her assets, including royalty payments from IMRO. IMRO is bound by the law. Therefore, in the absence of a valid will all royalties will be paid to those legally entitled.

The legal charges for making a will are quite small, and IMRO strongly advises that members make a will and recommend that a solicitor should be consulted as this is not always a straightforward process.

Successors to Provisional members are initially admitted to Provisional membership, whereas Successors to Associate or Full members are admitted to Associate membership (unless in the case of a deceased Full member the royalties over the last three years had fulfilled the criteria for Full Publisher membership). Once elected, Provisional Successor members are promoted to Associate membership status under the same criteria as living Writer members, and Associate Successor members are promoted to Full membership status in accordance with the criteria for Publisher members.

Unless a Successor member is elected, IMRO’s control of the rights in unpublished works will cease upon the expiry of the seven year period following the death of the last surviving interested party in the works. As regards published works, payment to the publishers will normally continue after the expiry of the seven year period, and include the former Writer share. The executors of the last member would no longer be entitled to receive that Writer share direct.

In conclusion, members should ensure that they have made a valid will specifically bequeathing their royalties (if appropriate), and to also include that a direction is given to close family and/or legal advisors to notify IMRO immediately after their death so that the above procedures can be put into effect swiftly.

Repertoire

1) The online works registration facility is available in the Member Services area of the website www.imro.ie. If the work is co-written, members must confirm to IMRO, via the online declaration, that they have notified all other contributors on the work that they are registering this work on their behalf and that all contributors agree to the share splits as indicated. Where members wish to notify several similar works, provided that the number of writers is the same and the contractual details and shares are identical, additional titles can be registered by using the Copy function on the work. Online works registrations are processed on a daily basis.

Via Paper Works Registration Forms

2) There are two types of paper forms which can be used to register works: a form for unpublished works and a form for published works. Unpublished work registration forms must be signed by all contributors on the work. Where members wish to notify several similar works, provided that the number of writers is the same and the contractual details and shares are identical, additional titles can be entered on the second page of the works registration form. Paper works registrations are processed on a weekly basis.

Work Amendments

Via Paper Works Registration Forms

3) Work amendments must be submitted to IMRO on paper works registration forms. All original and new contributors to the works, for whom shares are being updated, must sign and date the amended works registration form.

Duplicate Claims

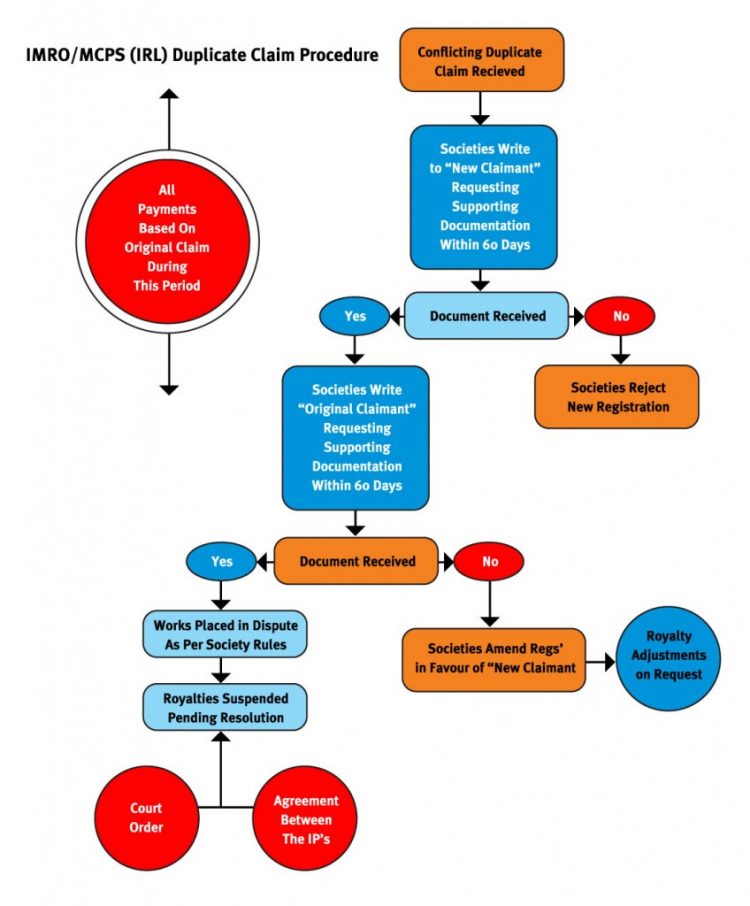

4) IMRO follows international best practice where counterclaims or disputes arise in relation to the ownership of musical works. Where a new copyright owner claim conflicts with an existing copyright owner claim, then the new claimant must be able to support this claim with documentation within 60 days before that claim can be accepted by IMRO. In the meantime, IMRO will continue to pay the original claimant. If the new claimant can document its claim, then the original claimant has 60 days to produce documentation for its claim. If the original claimant has not answered within 60 days, they will be notified that their claim has been replaced by the new claim. If both parties maintain claim and can supply supporting documentation, then either party can seek to have the works placed in dispute and the relevant shares suspended pending agreement. As per IMRO Rule 6, Board approval is required to place a work in dispute.

Writers should note…..

Published Works (i.e. works assigned to a publisher).

1) It is the responsibility of your publisher to register works you have assigned to that company. Published works should not be registered by the songwriter with certain exceptions. For example, a writer may wish to register works which are published abroad only or if there are works registration delays on the publisher’s side.

2) Writers who are under exclusive contract to a publisher should ensure that they advise their publisher of all new works as they are written to enable the publisher to register the works.

Unpublished Works (i.e. works not assigned to any publisher)

3) Should be registered with IMRO as soon as possible. Members can submit details of performance and recording activity online or when submitting the works to IMRO.

4) Each writer has a unique eleven digit CAE / IPI Number. This number should be entered in the appropriate field in order to correctly identify the writer. If you are co-writing with other IMRO members or members of affiliated societies, you should ensure that your co-writer’s CAE / IPI Number is also entered. If you are unsure of your CAE / Number, please contact IMRO Membership Services.

5) Members should not register their arrangements of copyright works as no share of royalties is allocated to an arranger in such cases. HOWEVER ARRANGEMENTS OF PUBLIC DOMAIN WORKS SHOULD BE REGISTERED.

6) If a composer has written incidental music for a non-musical play, the playwright’s name should not be shown in the author’s column. If songs have been written for the play, their individual titles and other details should be separately indicated, making it clear who wrote the words.

7) Specially commissioned works for a film, television or radio programme (or series) or any other audio-visual production should, wherever possible, be notified under the generic score title only (e.g. “Film X – Theme and Background Music”). It is not necessary to notify each individual cue employed in an audio-visual work, except where the nature of the cue differs substantially from the rest of the score (e.g. another interested party is involved, or the work is a commissioned song). If available, the producer’s music cue sheet for the production this should be sent directly to IMRO’s Distribution Team.

8) Performing shares must add up to exactly 100%. Mechanical shares must add up to exactly 100%.

9) In completing works registrations, members should indicate their preference for a US performing right society to collect royalties on their behalf; either ASCAP, BMI or SESAC. Where no choice is made by the member, the default choice is ASCAP.

Publishers should note…..

1) All contributors to the work must be identified on the works registration. CAE numbers should be entered in order to ensure the correct contributor is credited.

2) When notifying Co-Published works or ‘Split Copyrights’, you are not required to indicate contractual details of interests other than that part of the work you are notifying. However, all interested parties, (i.e. all the names of writers and publishers involved with the work) and applicable shares must be shown.

3) All forms should always be signed and dated – for publishers’ notifications the full name of the publisher and the capacity of the signatories should also be provided.

CAE Numbers The names of all writer and publisher members are entered, by the Society to which they belong, onto an international membership database, known as the IPI. This generates a unique CAE number for each society member. To protect confidentiality where writers register a pseudonym or where publishers trade under a different company name, a separate CAE number is allocated. Therefore, members may have more than one CAE number. In order to ensure work contributors are correctly identified, we request members to quote their CAE number when registering works and agreement details. If you are unsure of your CAE number, please contact IMRO Membership Services.

IMPORTANT When registering a work, whether by a publisher or writer/composer, the IMRO member is declaring their copyright ownership of that particular work. Therefore, it follows that in the event of a dispute regarding ownership of works, the legal obligation rests with the publisher or writer/composer to prove ownership.

Distribution

- 1 Introduction

- 2 Broadcast Royalties

- 2.1 Television

- National Television – General

- National Television – Advertising

- Local/Cable Television

- Cable Re-Transmission

- 2.2 Radio

- National /Quasi- National Radio – General

- National /Quasi- National Radio – Advertising

- Regional /Independent Local Radio – General

- Regional /Independent Local Radio – Advertising

- Regional/Independent Local Radio Advertising – Agency

- Digital Radio

- Community Radio

- 3 Cinema Royalties

- 3.1 Cinema – Mainstream

- 3.2 Cinema – Arthouse

- 3.3 Cinema Advertising

- 4 Live Royalties

- 4.1 Invoiced Live Events

- 4.2 Tours & Residencies Scheme

- 4.3 Live Music Survey

- 4.4 RTÉ Performing Groups

- 5 Background Music

- 5.1 Public Reception

- 5.2 Background Music – Shops & Bars – Recorded Music

- 5.3 Background Music – Hotels & Restaurants – Recorded Music

- 5.4 Commercial Discos

- 6 Digital Royalties

- 6.1 Music Downloads

- 6.2 Ringtones

- 6.3 Music Streaming

- 6.4 Video Streaming

- 7 Royalties from Overseas

- 8 International Standards

- 8.1 Inadequate Documentation

- 8.2 Unidentified Performances

- 8.3 Unidentified Commercials

- 8.4 Debit/Credit Adjustments

- 8.5 Suspense Amounts

- 8.6 Duplicate Claims/Dispute Works

1 Introduction

This document provides an overview of how IMRO distributes the royalties it collects on behalf of composers, authors and publishers. IMRO collects royalties from a range of sources and this document explains in detail how and when the royalties from each source are paid to the copyright owners. This document should be read by IMRO’s members, IMRO’s affiliates (performing right societies outside of Ireland with whom IMRO has a reciprocal agreement) and IMRO’s customers and is intended to make IMRO’s royalty distributions as transparent as possible. To make a distribution IMRO needs 2 key components- Royalty: The revenue collected from licensed users of music

- Data: Information related to the music usage by the licensed user

Under the terms of IMRO’s license agreements, many of IMRO’s customers are obliged to report to IMRO the musical works that they have used e.g. played on radio or at a live concert etc. These lists are brought into IMRO’s Distribution System and matched against the almost 14 million works held on IMRO’s database. IMRO then uses this information together with information provided by its members, affiliate societies and third parties to identify the copyright owners of each musical work used and to calculate the royalties due.

Wherever economically feasible, IMRO tries to ensure that the royalties received from each customer are paid directly on the basis of the musical works performed or broadcast by that user. Through the increase of electronic reporting from customers and the implementation of a new Distribution System, IMRO are processing ever increasing amounts of data in a cost-effective way. However, in some cases, the cost of processing the data will exceed the level of royalties collected; IMRO therefore uses a combination of techniques to distribute royalties.

Data Analysis

Census

When distributions are carried out on a census basis it means that the royalties received from an individual customer are distributed 100% across the music used and reported by that customer. Most television and radio station royalties are distributed this way.

Census/Sample

Some radio stations play most music from a ‘play-out’ system; however they will often have a range of specialist programmes that are returned manually. If a station’s royalties are distributed on the Census/Sample rate, it means that they are delivering full census reports for all automated programming (i.e. where music is played out using an automated/play-out system) and are on a sample rate for all programming not delivered via an automated system (i.e. incorporating specialist programming).

Sample

This is where royalties from an individual customer are distributed using a representative sample analysis of its logs. All sample data is chosen on a random basis using a software tool.

Analogies

Royalties for most performances given by recorded means (CD, juke boxes, background music devices etc.) are distributed by reference to statistical data, obtained from sources other than the licensees and which reflect contemporary patterns of music use. These can include sales charts, transmission logs from certain broadcasters, cinema operators, representative surveys etc.

Allocation Basis

Having processed the data from a particular provider the value of a given work can be calculated in one of two ways

Duration Basis

This method is used extensively in broadcast distributions. The net royalty for a radio station is divided by the total number of seconds of music broadcast in the distribution period to arrive at a ‘Point Value’ (the value of music per second). This ‘Point Value’ is then multiplied by the number of seconds reported by the broadcaster to calculate the royalty value for that particular song.

Example – Duration Basis

Under the terms of IMRO’s license agreements, many of IMRO’s customers are obliged to report to IMRO the musical works that they have used e.g. played on radio or at a live concert etc. These lists are brought into IMRO’s Distribution System and matched against the almost 14 million works held on IMRO’s database. IMRO then uses this information together with information provided by its members, affiliate societies and third parties to identify the copyright owners of each musical work used and to calculate the royalties due.

Wherever economically feasible, IMRO tries to ensure that the royalties received from each customer are paid directly on the basis of the musical works performed or broadcast by that user. Through the increase of electronic reporting from customers and the implementation of a new Distribution System, IMRO are processing ever increasing amounts of data in a cost-effective way. However, in some cases, the cost of processing the data will exceed the level of royalties collected; IMRO therefore uses a combination of techniques to distribute royalties.

Data Analysis

Census

When distributions are carried out on a census basis it means that the royalties received from an individual customer are distributed 100% across the music used and reported by that customer. Most television and radio station royalties are distributed this way.

Census/Sample

Some radio stations play most music from a ‘play-out’ system; however they will often have a range of specialist programmes that are returned manually. If a station’s royalties are distributed on the Census/Sample rate, it means that they are delivering full census reports for all automated programming (i.e. where music is played out using an automated/play-out system) and are on a sample rate for all programming not delivered via an automated system (i.e. incorporating specialist programming).

Sample

This is where royalties from an individual customer are distributed using a representative sample analysis of its logs. All sample data is chosen on a random basis using a software tool.

Analogies

Royalties for most performances given by recorded means (CD, juke boxes, background music devices etc.) are distributed by reference to statistical data, obtained from sources other than the licensees and which reflect contemporary patterns of music use. These can include sales charts, transmission logs from certain broadcasters, cinema operators, representative surveys etc.

Allocation Basis

Having processed the data from a particular provider the value of a given work can be calculated in one of two ways

Duration Basis

This method is used extensively in broadcast distributions. The net royalty for a radio station is divided by the total number of seconds of music broadcast in the distribution period to arrive at a ‘Point Value’ (the value of music per second). This ‘Point Value’ is then multiplied by the number of seconds reported by the broadcaster to calculate the royalty value for that particular song.

Example – Duration Basis

| Total Seconds of Music used by ‘Broadcaster 1’ in Distribution Period | 10,000,000 |

| Total net royalty paid by ‘Broadcaster 1’ for Distribution Period | €130,000 |

| Point Value’ (value per second) | €0.013 |

| Total duration (in seconds) reported by ‘Broadcaster 1’ for ‘Song A’. | 50,000 |

| Total royalty due to ‘Song A’ i.e. 50,000 * €0.013 | €650.00 |

| Total number of songs performed on a set-list | 20 |

| Total net royalty paid by ‘Promoter 1’ for that event | €1,000 |

| Point Value’ (value per play) | €50 |

| Total plays reported by ‘Promoter 1’ for ‘Song A’. | 2 |

| Total royalty due to ‘Song A’ i.e. 2 * €50 | €100 |

2 Broadcast Royalties

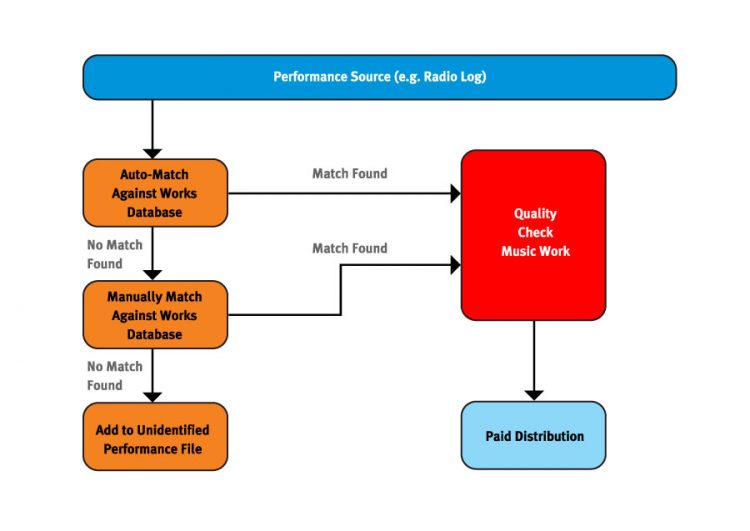

IMRO receives royalties from all Irish broadcasters. In the main the royalties from broadcasting are analysed on a Census basis where music duration is a key factor in determining the value of a royalty payment. The process for all surveyed broadcasters is as follows. * The Unidentified Performance file is made available to IMRO’s members and affiliates. (See Unidentified Performances section 8.2.)

* The Unidentified Performance file is made available to IMRO’s members and affiliates. (See Unidentified Performances section 8.2.)

2.1 Television

Television royalties are distributed by IMRO quarterly in April, July, October and December. Based on analysis of independently commissioned media monitoring data, IMRO policy is to split television royalties in the following manner:- 85% of net revenue is distributed to the music used in general programming

- 15% of net revenue is distributed across advertising data

National Television – General

There are 5 national TV stations in Ireland: RTÉ 1, RTÉ 2, TV3, TG4 and UTV Ireland. Each station returns complete transmission logs and these are analysed on a census basis. The royalties received from each station are distributed four times a year. A separate distribution pool is created from each station and the royalties received from that station are distributed across the music reports returned by that station. 85% of the net revenue received is distributed across ‘General Music’ i.e. the music used within all TV programmes, promos etc.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| RTÉ 1 TV – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| RTÉ 2 TV (2 Stations) – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| TV3 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| TG4 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & Dcember |

| UTV Ireland – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

National Television – Advertising

15% of the revenue in each station is reserved for an ‘Advertising Music’ pool as the music returns for adverts are processed separately.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| RTÉ TV (2 Stations) – Advertising Music – 15% of Net Revenue | Census | All are calculated on a duration basis | Quarterly. April, July, October & December |

| TV3 – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| TG4 – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| UTV Ireland – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

Local/Cable Television

There are very few indigenous cable-only stations in Ireland. Where economically feasible, IMRO’s policy is to distribute royalties on a census basis.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| 3e – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| 3e – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Setanta – General Music – 85% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Setanta – Advertising Music – 15% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

Cable Re-Transmission

IMRO licenses cable operators and satellite broadcasters for the cable re-transmission of foreign stations in Ireland. IMRO passes the royalties it collects for these stations to the society in the territory of original broadcast e.g. the royalties collected by IMRO for the re-transmission of BBC channels is passed to PRS which is then added to the main BBC PRS pools. The following is a selection of channels licensed by IMRO where the royalties are distributed by the societies in the original territory. <trBBC HDNick JnrSky Sports 3Film 4+1Sky Movies Sci Fi/Horror| BBC1 | ITV1 | Sky Sports 1 | E4 | Sky Movies Comedy |

| BBC2 | ITV2 | Sky Sports 2 | E4+1 | Sky Movies Drama |

| BBC3 | ITV3 | Sky Sports News | Discovery | Sky Movies Indie |

| BBC4 | ITV4 | Comedy Central 1 | Sky Living | Sky Movies Classics |

| CBeebies | C4 | Comedy Central +1 | Sky Living +1 | Sky Movies Premiere |

| CBBC | Sky 1 | Comedy Central Extra | MTV | Sky Movies Premiere + 1 |

| BBC News 24 | Sky News | Sky Two | E! | Sky Movies Family |

| BBC World | Nickelodeon | Sky Three/Pick | Film 4 | Sky Movies Modern Greats |

| Box TV | Disney | BT Sport | More 4 +1 | UKTV |

2.2 Radio

Radio royalties are distributed by IMRO quarterly in April, July, October and December. Based on analysis of independently commissioned media monitored data, radio royalties are split in the following manner- 85% of net revenue is distributed to the music used in general programming

- 15% of net revenue is distributed across advertising data

- For Independent Local Radio, the advertising revenue is further divided between In-House and Agency advertisements (see below)

National /Quasi- National Radio – General

There are 6 national/quasi-national radio stations in Ireland: RTÉ Radio 1, RTÉ Radio 2FM, Radió Na Gaeltachta, Lyric FM, Today FM and Newstalk. Each station returns complete transmission logs and these are analysed on a census basis. The royalties received from each station are distributed quarterly. A separate distribution pool is created for each station and the royalties received from that station are distributed across the music reports returned by that station.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| RTÉ: Radio 1 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| RTÉ: Lyric FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| RTÉ: RnaG – General Music – 100% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| RTÉ: 2FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Today FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Newstalk – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

National / Quasi – National Radio – Advertising

The advertising logs for each of these stations are processed separately. 15% of net revenue is reserved to fund each advertising distribution pool (with the exception of RnaG as it carries no advertising).| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| RTÉ: Radio 1 – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| RTÉ: Lyric FM – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| RTÉ: 2FM – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Today FM – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Newstalk – Advertising Music – 15% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

Regional /Independent local Radio – General

There are 30 Regional, Multi City and Independent Local Radio stations in Ireland. The royalties received from each station are distributed four times a year. A separate distribution pool is created from each station and the royalties received from that station are distributed across the music reports returned by that station.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| 4FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| 96FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Beat 102 103 FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| C103 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Clare FM – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 3 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| Dublin’s 98 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Sunshine FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| East Coast Radio – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| FM104 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Galway Bay FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Highland Radio – General Music – 85% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| i102-104 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| i105-107 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| KCLR – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| KFM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Limerick’s Live 95FM – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 4 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| LM/FM – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 2 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| Midland Radio 3 – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 2 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| MWR FM – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 4 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| Ocean FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| TXPhantom FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Q102 – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Radio Kerry – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 2 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| Radio Nova – General Music – 85% of Net Revenue | Census | Census for automated returns. | Quarterly. April, July, October & December |

| Red FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Shannonside/Northern Sound – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 3 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| South East Radio – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 6 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| Spin 103.8FM – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Spin South West – General Music – 85% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Spirit FM | Sample | One month per quarter. Calculated on a duration basis | Quarterly. April, July, October & December |

| Tipp FM – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 4 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

| WLR FM – General Music – 85% of Net Revenue | Census/ Sample | Census for automated returns. 2 day per month sample for non-automated. Calculated on a duration basis | Quarterly. April, July, October & December |

Regional / Independent Local Radio – Advertising

The advertising logs for each Regional /Local stations are processed separately. Two types of radio advertisements are reported by Independent Local Radio stations- In-House – in this case the station makes the advert itself and the data returned is of a very high quality and easily identified. 6% of net revenue is distributed across this data

- Agency – in this case, the advertising slots are bought through one of several central agencies and the adverts are typically for national or international products. 9% of net revenue from each of the following stations is used to fund the ILR Advertising Agency Pool (details given below)

| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| 4FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| 96FM – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Beat 102 103 FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| C103 – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Clare FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Dublin’s 98 – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Sunshine FM- In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| East Coast Radio – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| FM104 – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Galway Bay FM – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Highland Radio – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| i102-104 – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| i105-107 – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| KCLR – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| KFM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Limerick’s Live 95FM – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| LM/FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Midland Radio 3 – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| MWR FM – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Ocean FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| TXFM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Q102 – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Radio Kerry – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Radio Nova – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Red FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Shannonside/Northern Sound – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| South East Radio – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| Spin 103.8FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Spin South West – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Spirit FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

| Tipp FM – In-House Advertising Music – 6% of Net Revenue | Sample | 2 day per month sample. Calculated on a duration basis | Quarterly. April, July, October & December |

| WLR FM – In-House Advertising Music – 6% of Net Revenue | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

Regional / Independent Local Radio Advertising – Agency

To improve the accuracy of distributions relating to music used in radio advertising, 9% of revenue from all Local, Multi-City and Regional stations is reserved to fund the ILR Agency pool. The ad logs from a number of national stations are used as the basis on an analogy to distribute this revenue.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| ‘ILR Advertising Agency Pool’All Local, Regional and Multi-City Stations – Agency Advertising Music – 9% of Net Revenue | Analogy | Calculated on a duration basis using returns received from the following national stations: RTÉ Radio 1, 2FM, Newstalk, Today FM. | Quarterly. April, July, October & December |

Digital Radio

There are 6 digital radio stations in Ireland. As digital radio is in its infancy in Ireland and as the revenue received from this source is very modest no direct distributions take place.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| RTÉ Choice – General Music | Under Review | Currently the revenue received from this station is distributed pro-rata across the 4 RTÉ radio channels | Quarterly. April, July, October & December |

| RTÉ Junior – General Music | Under Review | Currently the revenue received from this station is distributed pro-rata across the 4 RTÉ radio channels | Quarterly. April, July, October & December |

| RTÉ Gold – General Music | Under Review | Currently the revenue received from this station is distributed pro-rata across the 4 RTÉ radio channels | Quarterly. April, July, October & December |

| RTÉ 2XM – General Music | Under Review | Currently the revenue received from this station is distributed pro-rata across the 4 RTÉ radio channels | Quarterly. April, July, October & December |

| RTÉ Pulse – General Music | Under Review | Currently the revenue received from this station is distributed pro-rata across the 4 RTÉ radio channels | Quarterly. April, July, October & December |

| RTÉ Chill – General Music | Under Review | Currently the revenue received from this station is distributed pro-rata across the 4 RTÉ radio channels | Quarterly. April, July, October & December |

Community Radio

There are a range of community radio stations and other stations that will from time to time receive temporary broadcast licenses. The revenue from these stations is distributed 50% across the RTÉ Radio 1/Lyric/RnaG General Music pool and 50% across the RTÉ 2FM General Music pools.3 Cinema Royalties

Cinema royalies are distributed by IMRO once a year in July. Based on extensive analysis of music usage within cinemas royalties are split on the following basis 1% of gross revenue is reserved and added to the Background Music Shops & Bars pool 95% of net revenue is distributed to the music used in the relevant films 5% of net revenue is distributed across advertising data3.1 Cinema – Mainstream

Mainstream cinema royalties are distributed on the basis of box office figures returned by Rentrak EDI. Rentrak EDI collects box-office information from all cinema operators in Ireland and compiles the official box-office charts. The relevant cue sheets are secured from IMRO’s members and from IMRO’s affiliates.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Mainstream Cinema – General Music | Census | This census is based on full annual box office figures received from Rentrak EDI. | Annually in July |

3.2 Cinema – Arthouse

Revenue from the IFI Cinema in Dublin makes up the Arthouse cinema pool. The royalties are distributed on the basis of performance logs returned by the IFI.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Arthouse Cinema – General Music | Sample | The sample is based on full annual returns received from the IFI cinema | Annually in July |

3.3 Cinema Advertising

Cinema advertising royalties are distributed on the basis of advertising logs provided by Wide Eye Media which has 100% site coverage in Ireland through all the major cinema exhibitors and through many independent operators.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Cinema – Advertising Music | Sample | Distributed on the basis of advertising logs returned by Wide Eye Media. The pool is made up of 5% revenue from both Mainstream & Arthouse cinema pools | Annually in July |

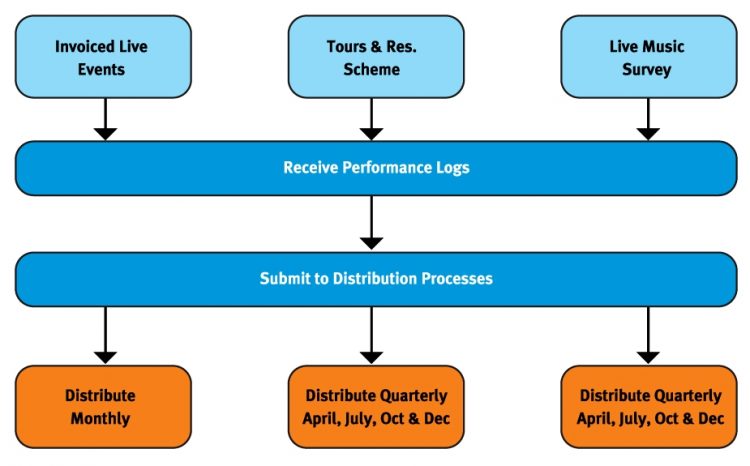

4 Live Royalties

As with broadcast royalties, IMRO strives to distribute as many live royalties as possible across actual usage data.

There are three main distribution pools for Live royalties. They are

- Invoiced Live Events

- Tours and Residencies Scheme

- Live Music Survey

4.1 Invoiced Live Events

Invoiced Live Events are gigs and concerts where a specific invoice has been raised for the event. On these occasions, IMRO will ring-fence the royalties collected for distribution across the actual set-lists used at the event.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Specifically Invoiced Live Events | Census | Per play basisGenerally these are larger invoiced events. 60% of net revenue is paid to the Headline Act and 40% to the Support Act/Acts. Where more than 8 acts play at an event it is classed as a festival and the royalties are split evenly between all acts.Costs (including Classical Concerts) are calculated on the following basis; the lesser of 25% gross royalty or (Total number of bands * €158.72) + €190.46. | Monthly |

4.2 Tours & Residencies Scheme

The Tours & Residencies scheme allows IMRO’s members and affiliates self-report all gigs they have performed in a quarter. The members and affiliates are required to submit both a Gig-List (a list detailing the date and venue of their performances) and a representative Set-List that includes all songs regularly performed.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Tours & Residencies | Self Reporting Scheme | Reported gigs receive €20 gross per venue per day within a 3 month reporting period. Set lists and gig lists are only accepted via the IMRO website. | Quarterly. April, July, October & December |

| Performances | Submission Type | Submission Deadline |

|---|---|---|

| January – March | Online submissions only | Mid-May |

| April – June | Online submissions only | Mid-August |

| July – September | Online submissions only | Mid-October |

| October – December | Online submissions only | Mid-February |

4.3 Live Music Survey

The royalties collected from all other live performances (i.e. not specifically invoiced or Tours and Residencies performances) are distributed on the basis of IMRO’s Live Music Survey. This survey of live performances in pubs, hotels & restaurants around the country is carried out on IMRO’s behalf by an independent market research company.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Live Revenue – All Other Venues | Sample | Live revenue from Bars, Hotels & Restaurants is paid based on a survey carried out by an independent market research firm. The survey is made up of 800 visits per annum to live gigs. 9 months of data is used in each quarterly distribution.Calculated on a Per Play basis. | Quarterly. April, July, October & December |

- The target of 800 visits per annum is set on a county by county basis (based on the number of venues in the county)

- The survey takes place throughout the year to account for seasonal changes

- Any reviewer should not see a performer more than once during any six month period

- Reviewers should not visit the same venue more than once a month

- All new reviewers are spot checked within first five reviews

- All reviewers completing over ten reviews are spot checked

4.4 RTÉ Performing Groups

The RTÉ Performing Groups is comprised of the following- RTÉ National Symphony Orchestra

- RTÉ Concert Orchestra

- RTÉ Vanbrugh Quartet

- RTÉ Philharmonic Choir

- RTÉ Cór na nÓg

| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| RTÉ Performing Groups | Census | Performances are weighted first by attendance figures and then by music duration. | Quarterly. April, July, October & December |

5 Background Music

The royalties from a range of sources for ‘background’ music is distributed over a number of different analogies. Generally background uses are made up of the public performance of Radio or Television in a premises or by mechanical means, e.g. CD, Tape, MP3 player etc. An analogy is a statistically sound and cost effective way to ensure that the correct mix of music is reflected in royalty payments to writers and publishers. These analogies are devised by first carrying out a survey of actual usage in the relevant type of premises e.g. Shops and Bars and then comparing the results with data already available to IMRO using an independently commissioned mathematical formula; this data will include sales charts, transmission logs from certain broadcasters etc. This comparison seeks to find degrees of similarity between the music captured in the actual survey and the data IMRO already has to hand. The analogies are reset every 5-7 years following a fresh survey of actual usage. The Background Music analogies are next due for review in 2018.5.1 Public Reception

This refers to the public performance of music by means of a television or radio by an IMRO customer.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Public Reception – TV & Radio | Analogy | Public Reception royalties collected for the use of TVs or Radios is added pro-rata to the relevant TV and Radio Stations (including re-transmitted cable & satellite stations where appropriate) | Quarterly. April, July, October & December |

5.2 Background Music – Shops & Bars – Recorded Music

Where an IMRO customer (shop owner or pub owner) pays a background mechanical tariff for the use of a CD player, MP3 player or juke-box etc. then the royalties are distributed via the Shops & Bars analogy.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Background Music – Shops & Bars | Analogy | Shops & Bars Background revenue is distributed on the basis of an analogy using selected radio logs and chart information. | Quarterly. April, July, October & December |

| 37.4% – Album charts for the period | |||

| 25% – Album charts for the previous period | |||

| 11.3% – Radio 1 logs for the period | |||

| 9.1% – Q102 logs for the period | |||

| 7.6% – 2FM logs for the period | |||

| 3.1% – WLR logs for the period | |||

| 2.9% – Highland Radio logs for the period | |||

| 1.7% – LMFM logs for the period | |||

| 1.3% – Galway Bay FM logs for the period | |||

| 0.6% – Clare FM logs for the period |

5.3 Background Music – Hotels & Restaurants – Recorded Music

Where an IMRO customer (hotel owner or restaurant owner) pays a background mechanical tariff for the use of a CD player, MP3 player or juke-box etc. then the royalties are distributed via the Hotels & Restaurants analogy.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Background Music – Hotels & Restaurants | Analogy | Hotel Background revenue is distributed on the basis of an analogy using selected radio logs and chart information. | Quarterly. April, July, October & December |

| 30% – RTÉ Radio 1 logs for the period | |||

| 28% – Album charts for the period | |||

| 18.9% – Album charts for the previous period | |||

| 17.5% – Q102 logs for the period | |||

| 2.8% – WLR logs for the period | |||

| 1.2% – Highland Radio logs for the period | |||

| 1% – LMFM logs for the period | |||

| 0.6% – Galway Bay FM logs for the period |

5.4 Commercial Discos

A specific analogy is used to distribute royalties collected from Commercial Discos.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| Commercial Discos | Analogy | Disco revenue is distributed on the basis of an analogy using selected radio logs and chart information. | Quarterly. April, July, October & December |

| 32% – Single Charts for the period | |||

| 20% – Music Week Club charts for the last 2 periods | |||

| 16% – Album Charts for the period | |||

| 16% – Spin FM logs for the period | |||

| 16% – 98FM logs for the period |

6 Digital Royalties

IMRO distributes royalties collected from a range of local MSPs (Music Service Providers). Given the emergent nature of this market and the large volume of data to be processed, general distribution policies are set but are reviewed on a case by case basis. IMRO has partnered with a number of affiliated societies (PRS, SACEM) to offer licenses to multi-territorial MSPs. Therefore for pan-European services, IMRO members will receive the majority of their digital royalties as overseas income.6.1 Music Downloads

All reported downloads from licensed MSPs are ‘auto-matched’. Unmatched downloads that have been sold three times or more will be ‘manually matched’. The total royalties collected will be distributed across all matched downloads.6.2 Ringtones

All reported ringtones from licensed Ringtone Providers are ‘auto-matched’. Unmatched ringtones that have been sold two times or more will be ‘manually matched’. The total royalties collected will be distributed across all matched ringtones.6.3 Music Streaming

All reported tracks that have received greater than a 200 streams in a quarter from licensed MSPs are ‘auto-matched’. Unmatched tracks that have been streamed 500 times or more will be ‘manually matched’. The total royalties collected will be distributed across all matched streams.6.4 Video Streaming

Given the extremely high volume of data returned by licensed on-demand streaming services, it is not practical to attempt to match all data.| Revenue Source | Analysis | Remarks | Distribution Frequency |

|---|---|---|---|

| RTÉ Player | Sample | The top 400 programmes per quarter are processed. Performances are weighted first by the total number of streams and then by the duration of music within the programmes. | Quarterly. April, July, October & December |

| iTunes Movies | Sample | The top 500 movies (with music titles) per quarter are processed. Performances are weighted first by the total number of streams and then by the duration of music within the movies. | Quarterly. April, July, October & December |

| XBox Movies | Sample | The top 100 movies (with music titles) per quarter are processed. Performances are weighted first by the total number of streams and then by the duration of music within the movies. | Quarterly. April, July, October & December |

| YouTube (Ireland) | Sample | The top 5000 videos (with music titles) per quarter are processed. Performances are weighted first by the total number of streams and then by the duration of music within the videos. | Quarterly. April, July, October & December |

| UPC TVOD (Transaction Video on Demand) | Sample | The top 100 movies (with music titles) per quarter are processed. Performances are weighted first by the total number of streams and then by the duration of music within the movies. | Quarterly. April, July, October & December |

| Netflix | Sample | The top 5000 titles per quarter are processed. Performances are weighted first by the total number of streams and then by the duration of music within the show / film. | Quarterly. April, July, October & December |

| UPV SVOD (Subscription Video on Demand) | Census | Calculated on a duration basis | Quarterly. April, July, October & December |

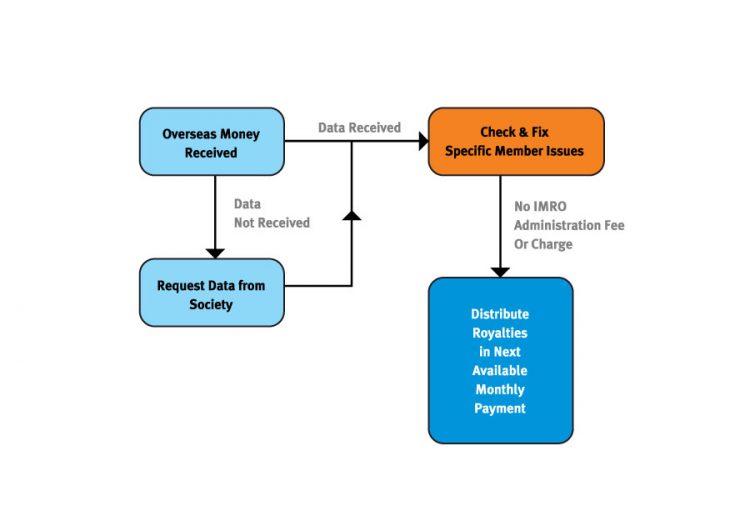

7 Royalties from Overseas

IMRO is committed to forwarding international royalties to its members in the shortest possible time. With 12 payment runs a year (January to December), IMRO is at the forefront internationally of providing the most frequent distribution of overseas royalties to its members.

All royalties received from an overseas sister society before the 20th of a given month are forwarded to our members by the 15th of the following month.

8 International Standards

IMRO is a member of CISAC (International Confederation of Societies of Authors and Composers), an umbrella group for collecting societies. As a member IMRO has signed up to CISAC’s professional rules; a code of conduct covering areas such as Governance, Membership and Transparency. In relation to Distribution, the Professional Rules set out a range of Binding Resolutions and Best Practices that IMRO fully adheres to.8.1 Inadequate Documentation

If at the time of distribution, there is inadequate documentation for a work that has been performed or broadcast but if one of the original rights holders can be identified as belonging to one of IMRO’s affiliated societies, then all the royalties accruing to the work must be forwarded to that affiliated society. That receiving society will then be responsible for carrying out the distribution and for providing IMRO with adequate documentation for future distributions. There is only one exception to the application of the Inadequate Documentation rule. That is where an identified original rights holder is an IMRO member. In that circumstance the royalties owing to the work will be placed in suspense and IMRO will contact its member to secure the correct documentation.8.2 Unidentified Performances

An unidentified use is a performance that cannot be matched to any documented work by IMRO and therefore cannot be distributed via the ‘Inadequate Documentation’ rule. In this scenario, the unidentified performances are placed on the UP File. The UP File is provided to affiliated societies in an agreed format and is also made available to IMRO’s members via the secure member area of the IMRO website. IMRO members who log-on to the website can search for any works that they believe were performed but have not received a payment for. Each unidentified performance on the UP file holds a notional value (the royalty it would have secured had it been identified at the time of distribution). A member can claim a performance by linking it to their relevant work and following validation by IMRO staff a payment will be made at the next available distribution.8.3 Unidentified Commercials

Unidentified Commercials refer to advertisements with music but where the music was unidentified at the time of distribution. In this scenario, the unidentified commercials are placed on the UC File. The UC File is provided to affiliated societies and also made available to IMRO’s members via the secure member area of the IMRO website. IMRO members who log-on to the website can search for any commercials that they believe were performed but have not received a payment for. Each unidentified commercial on the UC file holds a notional value (the royalty it would have secured had it been identified at the time of distribution). A member can claim an unidentified commercial by linking it to their relevant work and providing supporting information e.g. clock numbers. Following validation by IMRO staff a payment will be made at the next available distribution.8.4 Debit / Credit Adjustments

In the event of IMRO paying a work incorrectly or paying incorrect share splits on the work, then IMRO will carry out a Debit/Credit Adjustment. Following validation from IMRO staff, the royalties will be debited from the incorrect copyright owners and paid to the correct owner. Once notified of an incorrect payment, IMRO will carry out the necessary Debit/Credit Adjustment by the next available quarterly distribution. As per international standard, IMRO does not process adjustments for claims made more than 3 years after the original distribution.8.5 Suspense Amounts

If at the time of distribution, there is inadequate documentation for a work that has been performed or broadcast and none of the contributors can be identified, then the royalties due to that work are held in suspense i.e. the amount due to the work is reserved for a time to enable identification of the copyright owners. All suspense amounts are reviewed after a 6 month period to attempt to identify the correct copyright owners. Copyright owners who are successfully identified will receive a payment at the next available quarterly distribution. If after analysis, the correct copyright owner cannot be identified, then the royalties are returned to its relevant revenue pool for future distribution e.g. if the unidentified copyright owner featured on a work played on Today FM, then that unallocated royalty would be added to the Today FM pool at its next distribution.8.6 Duplicate Claims / Dispute Works

IMRO follows international best practice where counterclaims or disputes arise in relation to the ownership of musical works. Where a new copyright owner claim conflicts with an existing copyright owner claim, then the new claimant must be able to support this claim with documentation within 60 days before that claim can be accepted by IMRO. In the meantime, IMRO will continue to pay the original claimant. If the new claimant can document its claim, then the original claimant has 60 days to produce documentation for its claim. If the original claimant has not answered within 60 days, they will be notified that their claim has been replaced by the new claim. If both parties maintain a claim and can supply supporting documentation, then either party can seek to have the works placed in dispute and the relevant shares suspended pending agreement. As per IMRO Rule 6, Board approval is required to place a work in dispute. IMRO does not and will not arbitrate in the matter of disputes between interested parties and it is not IMRO’s responsibility to determine which of the claimant’s documentation is more correct or valid.

Document Control

IMRO Distribution Department IMRO Licensing Department IMRO Finance Department IMRO CEO IMRO Distribution Committee IMRO Board These policies were approved on the following dates:| Date/Time | Body | Note | |

|---|---|---|---|

| 02/12/2010 | IMRO Board | Revised ‘Census/Sample’ definition. | |

| 03/05/2011 | IMRO Board | Revised RTÉ TV & Radio policies; changes to cinema policies to use Rentrak EDI & Carlton Screen Advertising data; new Video Streaming policy. | |

| 14/09/2011 | IMRO Board | Revised RTÉ Performing Groups policy. | |

| 30/11/2011 | IMRO Board | Revised Tours & Residencies scheme; revised cable re-transmission policy; creation of ILR Agency Ad policy. | |

| 14/03/2012 | IMRO Board | Revised Music Streaming and RTÉ Player policies. | |

| 20/12/2012 | IMRO Board | Revised policies increasing distribution frequency for TV, Radio, Live, Background Music and Overseas Payments | |

| 20/02/2013 | IMRO Board | New policies for Spirit FM, Setanta Sports, iTunes Movies, X Box Movies | |

| 19/06/2013 | IMRO Board | Revised Cinema policy and various updates | |

| 18/09/2014 | IMRO Board | New policy for UPC TVOD | |

| 26/11/2014 | IMRO Board | Introduction of threshold for invoiced live events | |

| 17/09/2015 | IMRO Board | New policy for UPC SVOD, Netflix and UTV |

Licensing

Section D – Licensing

IMRO’s Methods of Licensing Public Performance

1. Public Performance

Through assignments from its own members and through affiliation agreements with foreign societies, IMRO owns or controls the public performance right in most of the copyright music played in Ireland. Its licence is therefore necessary for practically every public performance of copyright music in this country.

IMRO’s policy is to grant a licence to any prospective music user provided only that the person concerned is prepared to enter into the standard licence contract and pay the appropriate tariff royalty. The copyright in a work is infringed by a person who without the licence of the copyright owner, undertakes or authorises another to undertake a public performance of that work. The onus therefore lies on a music user and venue owner to obtain the permission of the copyright owner before public performances begin. Since IMRO controls the performing right in the musical works vested in it by copyright owners, it maintains nation-wide staff in the field to explain this obligation to unlicensed users of copyright music and to issue licences to them. Licences are also issued directly by the IMRO Head Office.

The tendency of music users not to seek an IMRO licence until approached by its IMRO staff means that the cost of issuing new licences is high. For this reason, unless the music user asks for a licence before being approached by IMRO staff. the royalty for the first year of a licence is 33.3% higher than the subsequent years charges.

IMRO is reluctant to litigate with music users who do not comply with the law and it takes all reasonable steps to ensure that music users are fully aware of their obligations. However, if a music user refuses to enter into a licence after the legal obligations have been fully explained to him/her, copyright infringement proceedings are begun in the Circuit Court. These proceedings seek an injunction preventing the performance of any of IMRO’s copyright repertoire in public until a licence is obtained and paid for, and IMRO also claims damages and costs.

2. IMRO’s Licences

IMRO’s licences cover both ‘live’ performances and performances by mechanical means, e.g. juke boxes, radio and television, video, record, CD, tape players, MP3 players, etc. Licences are in issue for numerous categories of premises, including cinemas, clubs, concert halls, discos, town halls, church halls, public houses, restaurants, shops, factories, universities, ships, aircraft, sports stadia, theatres and many others. Nearly 25,000 establishments hold an IMRO licence in Ireland.

In certain cases, permits (or one off licenses) are issued for the use of IMRO’s repertoire, or sometimes for specified works, either at a single performance or at a short series of performances at premises not licensed for those performances. If a copyright musical work is performed in public without the copyright owner’s consent then the copyright owner has a claim against not only the promoter of the performance but also the proprietor of the premises (unless he can show that he had no reason to believe that copyright infringement would take place) and the performers. It is not IMRO policy to grant licences to performers (other than to brass and military bands as such, for performances in public places). IMRO normally issues its licence to the proprietor of the venue concerned, so relieving the promoter of a musical entertainment at that venue from having to apply for a special permit licence. Promoters should make a point of ensuring that the proprietor holds an IMRO licence which will cover the occasion, when hiring a premises for a function involving the use of music.

Where a business operating multiple premises needs a licence, IMRO may issue a single licence to the Head Office of the company concerned. Royalties are then assessed depending on music usage and the number of premises involved. Since the licence is a contract it follows that the payment of royalties is an obligation enforceable by law. Those who remain in default after due reminders are issued, are sued in the appropriate courts as ordinary commercial debtors.

3. The Assessment and Payment of Royalties

Royalty charges payable by licensees are calculated under a series of carefully devised tariffs which normally take account of the type and frequency of the performances, the nature of the venue and other relevant circumstances. Many tariffs have been set after consultation with national associations representing the classes of music user to whom they apply.

As explained earlier, IMRO’s charges for the first year of a licence are 33.3% higher than the continuing royalty, unless the licensee sought that licence from IMRO before the relevant performances began.

IMRO’s principal tariffs are adjusted annually for inflation. The annual adjustment is by reference to movements in the Consumer Price Index.

Many IMRO licensees pay a flat annual charge which does not need to be adjusted from year to year, other than for inflation. These include most premises licensed only for background music. However, where the royalties are calculated as a percentage of admission receipts, or the number of employees (as in the case of factories and offices) or on a fluctuating number of live performances, dances, discos, or other events with music, then in fairness to both IMRO and the music user, the licensee may be asked to complete an annual return of the music usage so that the correct charge can be established.

Royalties are payable annually in advance. A licensee whose royalty is calculated and adjusted annually therefore pays, in the first year, an amount based on an estimate of the licensee’s music usage during the coming year. At the end of the year this payment is adjusted to the actual figure by reference to the returns sent in by him. For the ensuing year the licensee pays the equivalent of the royalty calculated for the previous year, that payment in turn is then adjusted twelve months later when the actual details can be ascertained. Licensees must inform IMRO of changes to performance particulars within latest 1 month of the end of year period to which the change relates, otherwise IMRO is not in a position to make an adjustment to the liability owed.

4. IMRO’s tariffs for Public Performance

Details of the scope and cost of IMRO tariffs may be obtained from the Licensing Department or on https://imro.ie/music-users/imro-ppi-tariffs/. Tariffs contain up-to-date information on the actual charges levied and many are subject to periodic review. Most tariffs provide for automatic increases in line with the cost of living increases.

Rights

Section E – Rights

Summary

The extent of the rights administered by IMRO on behalf of its members is regulated by detailed provisions in IMRO’s Articles of Association and in special directions issued by the Board of IMRO pursuant to the Articles. These definitions are long and somewhat complicated, but their general effect in practice is as follows. Subject to the exceptions explained in the next paragraph, IMRO administers the performing right in all its members’ musical works; and the term ‘performing right’ means the right (a) to perform a work in public, (b) to broadcast a work and to cause the work to be transmitted to subscribers to a diffusion service. IMRO also administers the film synchronisation right in any musical work specially written by a member for a film.

Exceptions (i) ‘Grand Right Works’ The rights administered by IMRO exclude what are usually referred to as ‘grand rights’. This expression is generally understood to refer to performances of dramatico-musical works and ballets.

In IMRO’s Articles of Association: – a dramatico-musical work means “an opera, an operetta, musical play, revue or pantomime, insofar as it consists of words and music written expressly therefor”

– a ballet means “a choreographic work having a story, plot or abstract idea, devised or used for the purpose of interpretation by dancing and/or miming, but does not include country or folk dancing, nor tap dancing, nor precision dance sequences”.

However, the performing right in dramatico-musical works and ballets is administered by IMRO when these works are performed by means of films which were made primarily for the purpose of exhibition in cinemas (and this control extends also to television broadcasting of such films). IMRO also controls performances of these works when given in public by means of radio or television sets (for example in a hotel lounge or a public house).

Television broadcasts of short ballets specially written for television up to a total duration of five minutes or of excerpts from existing ballets are also controlled by IMRO.

(ii) Excerpts from dramatico-musical works The extent to which excerpts from dramatico-musical works are controlled by the individual copyright owners and by IMRO respectively can be summarised as follows:-

a) Excerpts performed dramatically are always controlled by the individual copyright owner (except in the circumstances mentioned above in which IMRO would control a complete performance of such a work and, at the option of the member who is the owner of the copyright work, IMRO may administer the broadcasting right in a dramatic excerpt subject to certain conditions).

b) As regards excerpts performed non-dramatically public performances of these fall within IMRO’s control provided that they do not exceed 25 minutes duration and neither cover a complete act of the work nor consist of a ‘potted’ version of it. Non-dramatic excerpts in excess of those limits are controlled by the individual copyright owners. The same rules apply to television broadcasts (except that the maximum duration of excerpts controlled by IMRO is 20 minutes), and as regards radio broadcasts, all excerpts, however performed, fall within IMRO’s control except where they exceed the same limits as apply in the case of public performances (subject however to the additional proviso that the total duration of the excerpt(s) must not exceed 25% of the total length of the work).

(iii) Other exceptions The rights administered by IMRO also specifically exclude public performances (but not broadcasts) of music especially written for son-et-lumière productions and for dramatic productions in theatres, when performed in conjunction with such productions. In certain cases words written specially for commercial advertisements are also excluded from IMRO’s control.